Chapter - 1: Economic Outlook and Policy Challenges

ECONOMIC SURVEY & BUDGET 2016-17

This year's Survey comes in the wake of a set of tumultuous international developments:

- Brexit,

- political changes in advanced economies

- Two radical domestic policy actions: the GST and demonetisation.

INTRODUCTION

- The Economic Survey of 2014-15 spoke about the sweet spot for the Indian economy that could launch India onto atrajectory of sustained growth of 8-10 percent.

- Major challenges ahead:

- accelerating growth,

- expanding employment opportunities

- Achieving social justice.

THIS YEAR HAS BEEN MARKED BY SEVERAL HISTORIC ECONOMIC POLICY DEVELOPMENTS:

- On Domestic Side:- A constitutional amendment paved the way for the long-awaited and transformational goods and services tax (GST).

- Demonetisation of the large currency notes signalled a regime shift to punitively raise the costs of illicit activities.

- On International Front:- Brexit and the US elections may herald a tectonic shift,forebodingly laden with darker possibilities for the global, and even the Indian, economy.

DEMONETISATION

- A radical governance-cum-social engineering measure was enacted on November 8, 2016. The two largest denomination notes, Rs 500 and Rs 1000 -together comprising 86 percent of all the cash in circulation-were "demonetised.

- These notes were to be deposited in the banks by December 30.

- In other words,restrictions were placed on the convertibility of domestic money and bank deposits.

The aim of the action was fourfold:

- To curb corruption, counterfeiting, the useof high denomination notes for terrorist activities, and especially the accumulation of"black money", generated by income that has not been declared to the tax authorities.

- Earlier Efforts:- Special Investigation Team (SIT) in the 2014 budget,

- the Black Money Act, 2015;

- the Benami Transactions Act of 2016;

- the information exchange agreement with Switzerland,

- changes in the tax treaties with Mauritius and Cyprus, and the Income Disclosure Scheme

- In effect, the tax on illicit activities as well as on legal activities that were not disclosed to the tax authorities was sought to be permanently and punitively increased.

Short-term Costs of Demonetisation

- Short-term costs have taken the form of inconvenience and hardship, especially those in the informal and cash-intensive sectors of the economy who have lost income and employment.

- The benefits of lower interest rates and dampened price pressure may have cushioned the short-term macroeconomic impact.

Long-term Benefits

- Reduced corruption,

- greater digitalization of the economy,

- increased ?ows of financial savings, and

- greater formalization of the economy,

- All of which could eventually lead to higher GDP growth, better tax compliance and greater tax revenues.

NEEDED ACTIONS AFTER DEMONETISATION

- Remonetizing the economy expeditiously by supplying as much cash as necessary, especially in lower denomination notes.

- Complementing demonetization with more incentive-compatible actions such as bringing land and real estate into the GST,

- Reducing taxes and stamp duties, and ensuring that the follow-up to demonetisation does not lead to over-zealous tax administration.

MEDIUM TERM TRAJECTORY OF THE ECONOMY

The government has taken important steps over the past year:

- The transformational GST bill, which will create a common Indian market, improve tax compliance, boost investment and growth - and improve governance; the GST is also a bold new experiment in the governance of cooperative federalism.

- Overhauled the bankruptcy laws so that the "exit" problem that pervades the Indian economy.

- Codified the institutional arrangements on monetary policy with the Reserve Bank of India (RBI)

- Solidified the legal basis for Aadhaar, to realise the long-term gains from the JAMtrifecta (Jan Dhan-Aadhaar-Mobile)

OTHER IMPORTANT ACTIONS:

- The government enacted a package of measures to assist the clothing sector that by virtue of being export-oriented and labour intensive could provide a boost to employment, especially female employment.

- The National Payments Corporation of India (NPCI) successfully finalized the Unified Payments Interface (UPI) platform.

- Further FDI reform measures were implemented, allowing India to become one of the world's largest recipients of foreign direct investment.

These measures cemented India's reputation as one of the few bright spots in an otherwise grim global economy.

THREE MAJOR STRUCTURAL CHALLENGES:

- Inefficient redistribution,

- Strengthening state capacity in delivering essential services and regulating markets, and

- Dispelling the ambivalence about protecting property rights and embracing the private sector.

Inefficient Distribution

- The central government alone runs about 950 central sector and centrally sponsored schemes and sub-schemes which cost about 5 percent of GDP. Clearly, there are rationales for many of them. But there may be intrinsic limitations in terms of the effectiveness of targeting.

- The government has made great progress in improving redistributive efficiency over the last few years, most notably by passing the Aadhaar law, a vital component toward realizing its vision of JAM (The pilots forDirect Benefit Transfers in fertilizer representa very important new direction in this regard).

State Capacity

- On state capacity, delivery of essentialservices such as health and education, whichare predominantly the preserve of stategovernments, remains impaired.

- Whilecompetitive federalism has been a powerfulagent of change in relation to attractinginvestment and talent, it has been less inevidence in relation to essential servicedelivery.

Positive Development:

- The improvement ofthe public distribution system (PDS) inChhattisgarh, the incentivization of agriculturein Madhya Pradesh, reforms in the power sector in Gujarat which improved deliveryand cost recovery, the efficiency of socialprograms in Tamil Nadu, and the recent use oftechnology to help make Haryana kerosene free.

- Competitive populism needs a counterpart in competitive service delivery.

Property Rights and Private Sector

- Re-establishing private investment and exports as the predominant and durable sources of growth is the proximate macro-economic challenge.

GLOBAL CONTEXT

For India, three external developments are of significant consequence:

- The change in the outlook for global interest rates as a result of the US elections and the implied change in expectations of US fiscal and monetary policy will impaction India's capital lows and exchange rates.

- The medium-term political outlook for globalisation and in particular for the world's "political carrying capacity for globalisation" may have changed in the wake of recent developments. This changed outlook will affect India's export and growth prospects.

- Developments in the US, especially the rise of the dollar, will have implications for China's currency and currency policy.

- Internationally, allowing the currency to weaken in response to capital right risks creating trade frictions but imposing capital controls discourages FD Iand undermines China's ambitions to establish the Yuan as a reserve currency.

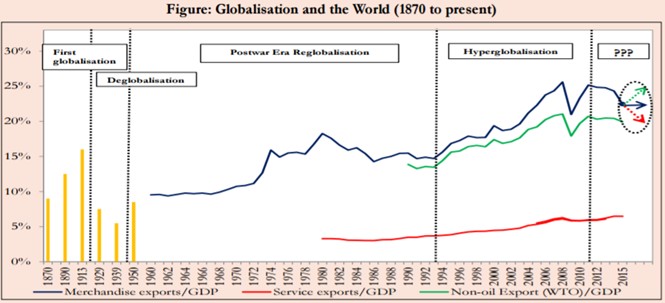

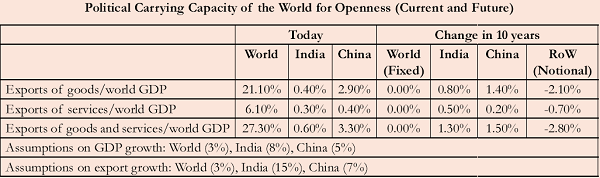

Political Carrying Capacity of the West for Openness and Impact on India

The question today is what is likely to happen, going forward represented by the three arrows: further globalisation, de-globalisation, or stagnation? These will have potentially important consequences for Indian exports and growth.

- The figure plots the trade-GDP ratio for the world since 1870 and highlights four phases. There were two phase of globalisation (1870-1914, 1945-1985), one phase of hyper-globalisation between 1985 and2008, and one phase of de-globalisation in the inter-war period.

- Political Carrying Capacity: the political carrying capacity of the world for globalisation can be defined as the world's export-to-GDP ratio. The latest figure for that is about 21 percent.

- From India's perspective, the political carrying capacity for globalisation is relevant not just for goods but also services.

- India's services exports growth will test the world's globalisation carrying capacity in services. Responses could take not just the form of restrictions on labour mobility but also restrictions in advanced countries on outsourcing.

- The political backlash against globalisation in advanced countries, and China's difficulties in rebalancing its economy, could have major implications for India's economic prospects.

REVIEW OF DEVELOPMENTS IN 2016-17

GDP and Inflation

- Real GDP growth in the first half of the year (2016-17) was 7.2 percent.

- The main problem was fixed investment, which declined sharply as stressed balance sheets in the corporate sector continued to take a toll on firms' spending plans.

- On the positive side, the economy was buoyed by government consumption, as the 7th Pay Commission salary recommendations were implemented.

- And by the long-awaited start of an export recovery as demand in advanced countries began to accelerate.

- The major highlights of the sectoral growth outcome of the first half of 2016-17 were:

- moderation in industrial and nongovernment service sectors;

- the modest pick-up in agricultural growth on the back of improved monsoon; and

- strong growth in public administration and defence services

INFLATION

- The Consumer Price Index (CPI)-New Series inflation, which averaged 4.9 per cent during April-December 2016, has displayed a downward trend since July when it became apparent that Kharif agricultural production in general, and pulses in particular would be bountiful.

- The decline in pulses prices has contributed substantially to the decline in

CPI inflation which reached 3.4 percent at end-December.

- WPI- The second distinctive feature has been the reversal of WPI inflation, from a trough of (-)5.1 percent in August 2015 to 3.4 percent at end-December 2016 on the back of rising international oil prices.

- Core inflation has, however, been more stable, hovering around 4.5 percent to 5 percent for the year so far.

External Sector

- Successfully weathered the sizeable redemption of Foreign Currency Non-Resident (FCNR) deposits in late 2016.

- The current account deficit has declined to reach about 0.3percent of GDP in the first half of FY2017.

- Foreign exchange reserves are at comfortable levels, having have risen from around US$350 billion at end-January 2016 to US$ 360 billion at end-December 2016.

- In part, surging net FDI in?ows, which grew from 1.7 percent of GDP in FY2016 to 3.2 percent of GDP in the second quarter of FY2017, helped the balance-of-payments.

- The trade deficit declined by 23.5 percent in April-December 2016 over corresponding period of previous year. During the first half of the fiscal year, the main factor was the contraction in imports, which was far steeper than the fall in exports.

- The improvement in exports appears to be linked to improvements in the world economy, led by better growth in the US and Germany.

- On the import side, the advantage on account of benign international oil prices has receded and is likely to exercise upward pressure on the import bill in the short to medium term.

- Net private remittances declined by $4.5 bn in the first half of 2016-17 compared to the same period of 2015-16, weighed down by the lagged effects of the oil price decline, which affected in?ows from the Gulf region.

FISCAL

- The central government is committed to achieving its fiscal deficit target of 3.5 percent of GDP this year.

- The most notable feature has been the over-performance of excise duties in turn based on buoyant petroleum consumption.

- Real consumption of petroleum products (petrol) increased by 11.2 percent during April-December 2016.

- Non-tax revenues have been challenged owing to shortfall in spectrum and disinvestment receipts but also to forecast optimism; the stress in public sector enterprises has also reduced dividend payments.

STATE GOVERNMENT

- State government finances are understress.

- The consolidated deficit of the states has increased steadily in recent years, rising from 2.5 percent of GDP in 2014-15 to 3.6 percent of GDP in 2015-16, in part because of the UDAY scheme.

- For the general government as a whole,there is an improvement in the fiscal deficit with and without UDAY scheme.

OUTLOOK FOR 2016-17 (Previous Financial Year)

Demonetisation affects the economy through three different channels:

- an aggregate demand shock because it reduces the supply of money

- an aggregate supply shock to the extent that economic activity relies on cash as an input (for example, agricultural production might be affected since sowing requires the use of labour traditionally paid in cash);

- an uncertainty shock because economic agents face imponderables related to the magnitude and duration of the cash shortage and the policy responses

Impact on supply of cash and money and interest rates

- It has reduced sharply, the supply of one type of money- cash-while increasing almost to the same extent another type of money-demand deposits.

- The price counterparts of this unusual aspect of demonetisation are the surge in the price of cash (inferred largely through queues and restrictions), on the one hand; and the decline in interest rates on the lending rate (based on the marginal cost of funds)

Macro-economic Consequences of Demonetisation

- Demonetisation coincided with the announcement of the US election results which also heralded a regime economic shift in the US.

- The most dramatic effect relates to interest rates. In almost all major countries, bond yields rose sharply after November 8, while In India, they had moved in the opposite direction.

- The decline in interest rates and the outlook triggered a large out?ow of foreign portfolio investment.

- Curiously, though, the impact on the exchange rate has been relatively modest, perhaps because of intervention by the RBI to stabilize the rupee.

IMPACT ON GDP

Five Broad indictors:

- Agriculture (Rabi) Sowing:

- Aggregate sowing of the two major rabi crops-wheat and pulses (gram)-exceeded last year's planting by 7.1 percent and 10.7 percent, respectively.

- Favourable weather and moisture conditions presage an increase in production.

- To what extent these favourable factors will be attenuated will depend on whether farmers' access to inputs-fertilizer, credit, and labour-was affected by the cash shortage.

- Indirect tax revenue, as a broad gauge of production and sales

- Indirect tax performance stripped of the effects of additional policy changes in 2016- 17, looks less robust than the headline number.Their growth has also been slowing but notmarkedly so after November 8.

- Auto sales, as a measure of discretionary consumer spending and two wheelers, as the best indicator of both rural and less af?uent demand

- Passenger car sales and excise taxesbear little imprint of demonetisation; propertymarkets in the major cities and sales of two-wheelers show a marked decline.

- Real credit growth

- Credit was already looking weak before demonetisation, and that pre-existing trend was reinforced.

- Real estate prices

- Showed a major decline.

REAL GDP GROWTH

- The balance of evidence leads to a conclusion that real GDP and economic activity has been affected adversely, but temporarily by demonetisation.

- Given the uncertainty, we provide a range: a ¼ percentage point to 1 percentage point reduction in nominal GDP growth relative to the baseline of 11¼ percent; and a ¼ percentage point to ½ percentage point reduction in real GDP growth relative to the baseline of estimate of about 7 percent.

- Over the medium run, the implementation of the GST, follow-up to demonetisation, and enacting other structural reforms should take the economy towards its potential real GDP growth of 8 percent to 10 percent.

- Recorded GDP growth in the second half of FY2017 will understate the overall impact because the most affected parts of the economy-informal and cash-based- are either not captured in the national income accounts or to the extent they are, their measurement is based on formal sector indicators.

- The impact on the informal sector will, however, be captured insofar as lower incomes affect demand for formal sector output, for example, two-wheelers.

Conclusion:

- It is likely, for example, that uncertainty caused consumers to postpone purchases and firms to put off investments in the third quarter. But as the economy is remonetised and conditions normalise, the uncertainty should dissipate and spending might well rebound toward the end of the fiscal year.

- Finally, demonetisation will afford an interesting natural experiment on the substitutability between cash and other forms of money. Demonetisation has driven a sharp and dramatic wedge in the supply of these two: if cash and other forms are substitutable, the impact will be relatively muted; if, on the other hand, cash is not substitutable the impact will be greater.

OUTLOOK FOR 2017-18

REAL GDP: Important Components: the components of aggregate demand: exports, consumption, private investment and government.

Exports:

- India's exports appear to be recovering, based on an uptick in global economic activity.

- The IMF's January update of its World Economic Outlook forecast is projecting an increase in global growth from 3.1 percent in 2016 to3.4 percent in 2017.

Private Consumption:

- The outlook for private consumption is less clear. International oil prices are expected to be about 10-15 percent higher in 2017 compared to 2016, which would create a drag of about 0.5 percentage points.

- On the other hand, consumption is expected to receive a boost from two sources: catch-up after the demonetisation-induced reduction in the last two quarters of 2016-17; and cheaper borrowing costs, which are likely to be lower in 2017 than 2016 by as much as 75 to 100 basis points. As a result, spending on housing and consumer durables and semi-durables could rise smartly.

Private Investment:

- Since no clear progress is yet visible in tackling the twin balance sheet problem, private investment is unlikely to recover significantly from the levels of FY2017.

Government (Public) Investment:

- It would depend on the stance of fiscal policy next year, which has to balance the short-term requirements of an economy recovering from demonetisation against the medium-term necessity of adhering to fiscal discipline-and the need to be seen as doing so.

Conclusion:

- Putting these factors together, we expect real GDP growth to be in the 6¾(6.75%) to 7½ (7.50) percent range in FY2018.

Risk to the Forecast of real GDP for 2017-18:

- The extent to which the effects of demonetisation could linger into next year

- Currency shortages also affect supplies of certain agricultural products, especially milk (where procurement has been low), sugar (where cane availability and drought in the southern states will restrict production), and potatoes and onions (where sowings have been low).

- Vigilance is essential to prevent other agricultural products becoming in 2017-18 what pulses were in 2015-16.

- Geopolitics could take oil prices up further than forecast

- The ability of shale oil production to respond quickly should contain the risks of a sharp increase, but even if prices rose merely to $60-65/barrel the Indian economy would nonetheless be affected by way of reduced consumption; less room for public investment; and lower corporate margins, further denting private investment.

- Trade Tensions:

- There are risks from the possible eruption of trade tensions amongst the major countries, triggered by geo-politics or currency movements. This could reduce global growth and trigger capital right from emerging markets.

- The one significant upside possibility is a strong rebound in global demand and hence in India's exports.

FISCAL OUTLOOK

The fiscal outlook for the central government for next year will be marked by three factors.

- Tax/GDP ratio: the increase in the tax to GDP ratio of about 0.5 percentage points

- There will be a fiscal windfall both from the high denomination notes that are not returned to the RBI and from higher tax collections as a result of increased disclosure under the Pradhan Mantra Garib Kalyan Yojana (PMGKY).

- GST: A third factor will be the implementation of the GST. It appears that the GST will probably be implemented later in the fiscal year. The transition to the GST is so complicated from an administrative and technology perspective that revenue collection will take some time to reach full potential. Combined with the government's commitment to compensating the states for any shortfall in their own GST collections (relative to a baseline of 14 percent increase), the outlook must be cautious with respect to revenue collections.

- In addition, muted non-tax revenues and allowances granted under the 7th Pay

- Commission could add to pressures on the deficit.

THE MACROECONOMIC POLICY STANCE FOR 2017-18

- The banking system will benefit from a higher level of deposits. Thus, market interest rates-deposits, lending, and yields on g-secs-should be lower in 2017-18 than 2016-17. This will provide a boost to the economy (provided, of course, liquidity is no longer a binding constraint).

- Of course, any sharp uptick in oil prices and those of agricultural products, would limit the scope for monetary easing. The central government fiscal deficit declining from 4.5 percent of GDP in 2013- 14 to 4.1 percent, 3.9 percent, and 3.5 percent in the following three years. But fiscal policy needs to balance the cyclical imperatives with medium term issues relating to prudence and credibility.

Use of Windfall Gain:

- One key question will be the use of the fiscal windfall (comprising the unreturned cash and additional receipts under the PMGKY) which is still uncertain.

- It should be deployed to strengthening the government's balance sheet rather than being used for government consumption, especially in the form of programs that create permanent entitlements.

- the best use of the windfall would be to create a public sector asset reconstruction company (discussed in Chapter 4) so that the twin balance sheet problem can be addressed, facilitating credit and investment revival; or toward the compensation fund for the GST that would allow the rates to be lowered and simplified; or toward debt reduction.

Important Reforms Target in 2017-18

- Perhaps the most important reforms to boost growth will be structural. In addition to those spelt out in Section 1-strategic disinvestment, tax reform, subsidy rationalization-it is imperative to address directly the twin balance sheet problem.

Labour Reform

- Whether they want to make their own contribution to the Employees' Provident Fund Organisation (EPFO); whether the employers' contribution should go to the EPFO or the National Pension Scheme; and whether to contribute to the Employee State Insurance (ESI) or an alternative medical insurance program.

- There could be a gradual move to ensure that at least compliance with the central labour laws is made paperless, presence-less, and cashless.

On Expenditure Side:

- The Existing government programs suffer from poor targeting.

- Issue A:the provision of a universal basic income

- Issue B (Procedural): a standstill on new government programs, a commitment to assess every new program only if it can be shown to demonstrably address the limitations of an existing one that is similar to the proposed one; and a commitment to evaluate and phase down existing programs that are not serving their purpose.

OTHER ISSUES

Redistribution: Universal Basic Income (UBI) as a radical new vision

- The central government alone runs about 950 central sector and centrally sponsored sub-schemes which cost about 5 percent of GDP.

- Evidence of Misallocation:

- The districts in States having the largest share of poor facing the greatest shortfall in allocation of funds.

- Alternative Solution to this Problem: UBI

- A UBI has the merit that it will not necessarily be driven by take-up capability from below but given from above to all the deserving.

- It is less likely to be prone to exclusion errors. And by directly transferring money to bank accounts, and circumventing multiple layers of bureaucracy, the scope for out-of system leakages (a feature of PDS schemes) is low. Of course, there are considerable implementation challenges which will have to be debated and addressed.

Exchange rate policy: Vigilance and new ways of monitoring

- Given India's need for exports to sustain a healthy growth rate, it is important to track India's competitiveness.

- India's Competitors in Manufacturing and Services:

- A second reason to review India's competitiveness is the rise of countries such as Vietnam, Bangladesh, and the Philippines that compete with India across a range of manufacturing and services.

India's Exchange Rate Competitiveness:

- The indices of real effective exchange rates suggest that since the crisis of 2013, India's rupee has appreciated by 19.4 percent (October 2016 over Jan 2014) according to the IMF's measure, and 12.0 percent according to the RBI's measure.

- Both these indices could be misleading.

- The RBI's measure for example assigns an unusually high weight to the United Arab Emirates as it is a major source of India's oil imports, and a transhipment point for India's exports.

- But little of this trade has to do with competitiveness.

- Heavy weight is given to the euro, even though it is really Asian countries, not Europe, that are India's main competitors.

A New Real Exchange Rate Index:

- It focuses on India's manufacturing competitors.

- Essentially, we give a higher weight to those countries that have become highly competitive in manufacturing since the Global Financial Crisis, measured by their change in global export market share.

- The surprising finding is that the IMF and RBI indices overstate the rupee's appreciation since 2014, largely because they give such a large weight to the euro, which has been exceptionally weak.

- In one (REERASIA-M) we given moderately high weight, and in a second (REER-ASIA-H) significantly greater weight, to India's competitors (China, Vietnam, the Philippines) that have gained market share since 2010.

- India has managed to maintain export competitiveness despite capital inflows and inflation that has been greater than in trading partners. Reflecting this, India's global market share in manufacturing exports has risen between 2010 and 2015.

The policy implication:

- Policy implication is that if India is concerned about competitiveness and the rise of exporters in Asia, it should monitor an exchange rate index that gives more weight to the currencies of these countries.

TRADE POLICY

- The environment for global trade policy has probably undergone a paradigm shift in the aftermath of Brexit and the US elections.

- This can be exacerbated by the appreciation in dollar.

- Emergence of Protectionist Tendencies:

- India and other emerging market economies must play a more proactive role in ensuring open global markets.

- A vacuum in international trade leadership is being created which must be filled with voices and in?uences such as India's that favour open markets. This will, of course, require that India also be more willing to liberalize its own markets, a greater "openness to its own openness."

Two Opportunities: Promotion of Labour Intensive Exports

- The first, on the need to promote labour-intensive exports, India could more proactively seek to negotiate free trade agreements with the UK and Europe. The potential gains for export and employment growth are substantial.

Strengthening of WTO:

- US retreat from regional initiatives such as the Trans-Pacific Partnership (TPP) in Asia and the Trans-Atlantic Trade and Investment Partnership (TTIP) with the EU; it is possible that the relevance of the World Trade Organization might increase.

- Reviving the WTO and multilateralism more broadly could be proactively pursued by India.

Climate Change and India:

- The Paris Agreement on climate change in December 2015 has been one of the shining recent examples of successful international cooperation.

- There is universal agreement that a key component to tackling climate change will be to price carbon.

How has India fared on this score?

- The increase in petrol tax has been over 150 percent in India.

- As a result, India now outperforms all the countries except those in Europe in terms of tax on petroleum and diesel.

- Having decisively moved from a regime of carbon subsidies, it is now de facto imposing a carbon tax on petroleum products at about US$150 per ton, which is about 6 times greater than the level recommended by the Stern Review on Climate Change.

- Pattern of Fossil Fuel Use in Overall Energy Consumption of India.

- India's reliance on fossil fuels remains well below China (the most relevant comparator) but also below the US, UK and Europe at comparable stages of development.

ENSURING WOMEN'S PRIVACY

- Lack of Accessibility to Sanitation Facilities

- The disproportionate burden that falls on women and girls due to deficiencies in sanitation facilities.

- This burden on women can take several forms:

- threat to life and safety while going out for open defecation,

- reduction in food and water intake practices to minimize the need to exit the home to use toilets,

- Polluted water leading to women and children dying from childbirth-related infections, and a host of other impacts.

- Why sanitation is so important for women?

- Women's personal hygiene is therefore important not just for better health outcomes but also for the intrinsic value in conferring freedom that comes from having control over their bodies, a kind of basic right to physical privacy.

- Recent data shows that about 60 percent of rural households 89 per cent of urban households have access to toilets - a considerably greater coverage than reported by the Census 2011.

The Disproportionate Burden on Women

- Households without toilets:

- Covering of Large Distance: 76 percent of women had to travel a considerable distance14 to usethese facilities.

- Physical assault: 33 percent of the women have reported facing privacy concerns and assault while going out in the open.

- Reduction in Food and Water intake: The number of women who have reduced consumption of food and water are 33 percent and 28 percent respectively of the sample.

- Snake Biting: that women and men going out into the open have to cope also with exposure to natural elements, snakebites, etc

- Household with toilets:

- In households with toilets, women report far greater use of these in-home facilities than men, suggesting that there may be a greate demand amongst women.

- What this pattern of usage suggests is that women and girl-children could take a key leadership role to play in Swachh Bharat's objective of creating defecation free communities, by nudging men and boys of the household to change their own defecation behaviours.

INDIA'S SOON-TO-RECEDE DEMOGRAPHIC DIVIDEND

- 2016 was a turning point in global demographic trends. It was the first time since 1950 that the combined working age (WA) population (15-59) of the advanced countries declined.

- India, however, seems to be in a demographic sweet spot with its working-age population projected to grow by a third over the same period; always remembering that demography provides potential and is not destiny.

Demographic Dividend and Economic Growth:

- Economic research in the last two decades has suggested that the growth surges in East Asia may have been driven by demographic changes.

- Younger populations are more entrepreneurial (adding to productivity growth); tend to save more, which may also lead to favourable competitiveness effects and have a larger fiscal base because of economic growth and because there are fewer dependents (children and elderly) for the economy and government to support

- The specific variable driving the demographic dividend is the ratio of the working age to non-working age (NWA) population.

Distinctive Indian Demography

- Three distinct features about the Indian demographic profile that have key implications for the growth outlook of India and the Indian states.

- India's demographic cycle is about 10-30 years behind that of the other countries.

- In India, however, the decline in TFR has been much more gradual. India might be able to sustain high levels of growth (on account of the demographic dividend) for a longer time.

- There is a clear divide between peninsular India (West Bengal, Kerala,Karnataka, Tamil Nadu and Andhra Pradesh) and the hinterland states (Madhya Pradesh,Rajasthan, Uttar Pradesh, and Bihar). The peninsular states exhibit a pattern that is closer to China and Korea, with sharp rises and declines in the working age population. In contrast, the hinterland states will remain relatively young and dynamic, characterized by a rising working age population for some time plateauing out towards the middle of the century.

- This divide in the WA/NWA ratio of the peninsular and the hinterland states can be traced to the difference in their levels of TFR.

- Demographically speaking, therefore, there are two India’s, with different policy concerns: a soon-to-begin-ageing India where the elderly and their needs will require greater attention; and a young India where providing education skills, and employment opportunities must be the focus.

GROWTH CONSEQUENCES

This demographic pattern will have two important growth consequences:

- First, it seems that the peak of the demographic dividend is approaching fast for India. That peninsular India will peak around 2020 while hinterland India will peak later around 2040. India will approach, within four years, the peak of its demographic dividend. (Note: this does not mean that the demographic dividend will turn negative; rather, the positive impact will slow down.)

- The second growth consequence relates to the distributional impacts across India. One way of assessing this is to compare the demographic dividend for the different states in terms of extra growth against their current level of per capita GDP. The good news is that there is a negative relationship, which means that on average the poorer states today have more of a growth dividend ahead of them. This means the demographic dividend could help income levels across states converge.

- Bihar, Jammu and Kashmir, Haryana, and Maharashtra are positive outliers in that they can expect a greater demographic dividend over the coming years than would be suggested by their current level of income. This extra dividend will help Bihar converge.

- On the other hand, Kerala, Madhya Pradesh, Chhatisgarh, and West Bengal are negative outliers: their future dividend is relatively low for their level of income.

Ch-2: The Economic Vision For Precocious, Cleavaged India

Ch-3: Demonetization: to Deify or Demonize?

Ch-4: The Festering twin Balance Sheet Problem

Ch-05: Fiscal Framework: The world is changing, should India change Too

Ch-06: Fiscal Rules: Lessons from the states

Ch-7: Clothes and Shoes: Can India Reclaim Low skill Manufacturing

Ch-8: Review of Economic Developments

Ch-09: Universal Basic Income: A conversation with and within the Mahatma

Ch-10 : Income, Health, and Fertility: Convergence Puzzles

Ch-11: One Economic India: For Goods and in the Eyes of the Constitution

Ch-12: India on the Move and Churning new evidences

Ch-13: The Other India’s: Two Analytical Narratives (Redistributive and Natural Resources) on States Development

Ch-14: From Competitive Federalism to Competitive sub federalism: cities as

dynamos